read: 688 time:2022-07-15 11:16:51 from:

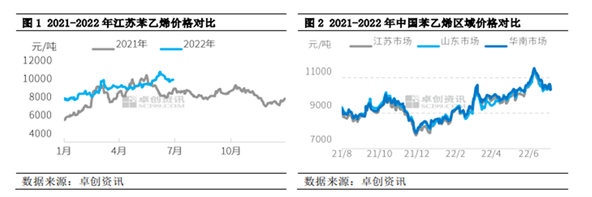

Styrene market in the first half of 2022 showed an oscillating upward trend, the average price of styrene market in Jiangsu was 9,710.35 yuan / ton, up 8.99% YoY and up 9.24% YoY. The lowest price in the first half of the year appeared at the beginning of the year 8320 yuan / ton, the highest price appeared in early June 11470 yuan / ton, an amplitude of 37.86%. Fundamentally, the supply of styrene in the first half of 2022 showed a trend of first increase and then decrease, demand showed a gradual increase in the trend of the overall supply and demand structure for the progressively tighter state.

The "Black Swan" events occur frequently in the first half of the year to a new high of nearly two years

The main reason for the rise in styrene prices in the first half of the year from the macro perspective is the result of global inflation, the center of gravity of commodities have risen, reflected in styrene is the cost support from the raw material side (crude oil), pure benzene in the first half of the year, their own resources are also tight, continue to rise; from the styrene fundamentals are mainly with the first half of the styrene domestic and foreign production units in the centralized maintenance period, while the unplanned supply reduction is also more More, the price difference between domestic and foreign markets makes styrene exports increased, but also to fill part of the weak domestic demand on the price of the negative impact.

From the perspective of different regions of styrene, there are new units coming on stream in South China and Shandong in 2022, but along with unplanned shutdowns of large units in the region, the regional supply and demand structure is also changing in phases. South China and Jiangsu market from the discount to ascending, and Shandong market from the obvious discount to Jiangsu market to the spread gradually narrowed.

The first half of the year was cost "kidnapped" high cost of styrene prices determine the height

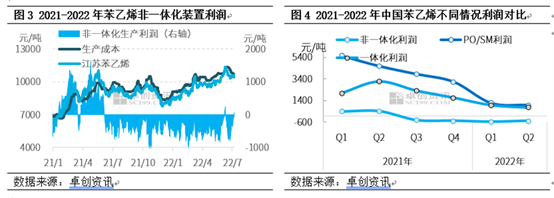

Styrene non-integrated plant profit in the first half of 2022 at -509 yuan / ton, down 226.30% from 403 yuan / ton in the same period last year; the first half of the basic loss-oriented, only the first half of June profits briefly turned positive.

2022 after the Spring Festival international oil prices all the way up, driving pure benzene strong higher, coupled with the first half of the pure benzene market fundamentals tight, pure benzene inventory continued to decline, the price performance is relatively firm, pure benzene and styrene spread gradually narrowed, once narrowed to the level of five or six hundred, but also make styrene producers began to fall in the loss pressure negative / shutdown, but also the first half of the styrene supply is not as expected growth.

Domestic production growth is less than expected foreign demand increased beyond expectations

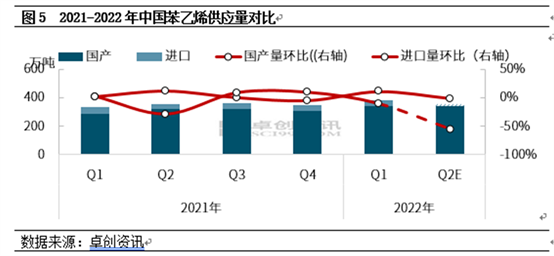

In the first half of 2022, styrene is expected to be put into production within the large installations have basically been put into production, as of July, China styrene has been put into production 2.88 million tons.

The new styrene plants are coming on stream roughly as planned, but the domestic production growth rate is less than expected, mainly because on the one hand, some plants have started to shut down for a long time against the background of long-term losses in styrene; on the other hand, there are more unplanned shutdowns of styrene plants in the first half of the year. Styrene imports in the first half of the year also declined to some extent, with the gradual commissioning of domestic installations, with styrene imports in January-May 2021 at 730,400 tons and January-May 2022 at 522,100 tons, down 28.51% year-on-year.

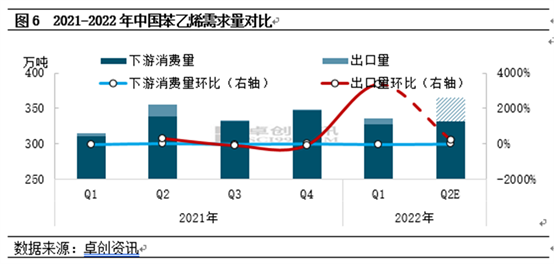

In the first half of 2022, styrene domestic demand performance is lukewarm, from the Spring Festival, the market began to look forward to demand recovery, until July, the terminal demand did not see a significant increase, especially in March-April by force majeure, the recovery in demand was interrupted, or ultimately the terminal real estate, home appliances demand is weak, the transmission to the upstream raw material link, is the downstream prices do not go up, finished goods inventory is still increasing The reason for the interruption of demand recovery is ultimately the weak demand for real estate and home appliances. According to Zhuo Chuang data testing, the first half of 2022 styrene downstream consumption in 6.597 million tons, a small increase of 2% over the same period last year, down 3% compared to the fourth quarter of last year. The first half of the styrene export performance continues to shine, export data has hit a record high, 2021 China's styrene exports in 234,900 tons, an increase of 770.00%. 2022 January-May exports in 342,200 tons, an increase of 80.42%. The reason for the growth of exports is on the one hand, more planned and unplanned maintenance of overseas installations, supply reduction, there is a demand gap; on the other hand, in the inflationary environment, there is a difference in price increases at home and abroad, there is a certain arbitrage space exists.

The second half of the supply and demand structure or from tight to loose prices are expected to be high before and after the low

Fundamentals, styrene in the third quarter there are no new devices put into operation, the fourth quarter there are Guangdong Jieyang 800,000 tons / year (October-November), Lianyungang Petrochemical 600,000 tons / year (October), Zibo Junchen (formerly Qi Wanda) 500,000 tons / year (mid-October), Zhejiang Petrochemical 600,000 tons / year (fourth quarter), Anqing Petrochemical 400,000 tons / year (the end of the year) a total of 2.9 million tons / year device is scheduled to go into operation. In the third quarter, there are still Zhejiang Petrochemical 1.2 million tons / year plant in August planned maintenance of about 40 days; China Shell II plans to replace the catalyst at the end of July and early August, so it is expected that the supply of styrene in the third quarter is expected to increase, but slowly. The downstream in the third quarter there is a batch of devices planned to put into operation, if the production is smooth, for styrene demand is a support, but the current downstream industry profits are loss, for the downstream of the new device is expected to bring the impact of the production schedule. Overall, the supply and demand structure of styrene is expected to turn from tight to loose.

From the cost side, the market for the international oil prices are also very different, the oil market confusion, adding to the uncertainty of the styrene market in the second half of the year, if the center of gravity of oil prices in the third quarter failed to fall widely, and the third quarter pure benzene supply and demand is expected to remain tight, then the styrene market in the third quarter may not be particularly pessimistic, some market participants based on the second half of the macroeconomic concerns and pessimism about the real estate industry. For the time being, the market is short attitude. Into the fourth quarter, international oil prices have greater downward pressure, and the new pure benzene device is expected to have stabilized production, increased supply, weakening cost support, coupled with the fourth quarter styrene industry demand will have further weakening is expected, the price center of gravity or expected to further decline.

Source: China Universe Information

*Disclaimer: The content contained in this article comes from the Internet, WeChat public number and other public channels, we maintain a neutral attitude towards the views in the article. This article is for reference and exchange only. The copyright of the reproduced manuscript belongs to the original author and the institution, if there is any infringement, please contact the chemical easy world customer service to delete.

Jincheng Petrochemical's 300000 ton polypropylene plant successfully trial production, 2024 polypropylene market analysis

The ABS market remains sluggish, what is the future direction?

Market differentiation of bisphenol A intensifies: prices rise in East China, while prices generally decline in other regions

The production method and process flow of silicone acrylic lotion, and what are the common raw materials