read: 914 time:2022-04-01 14:08:25 from:

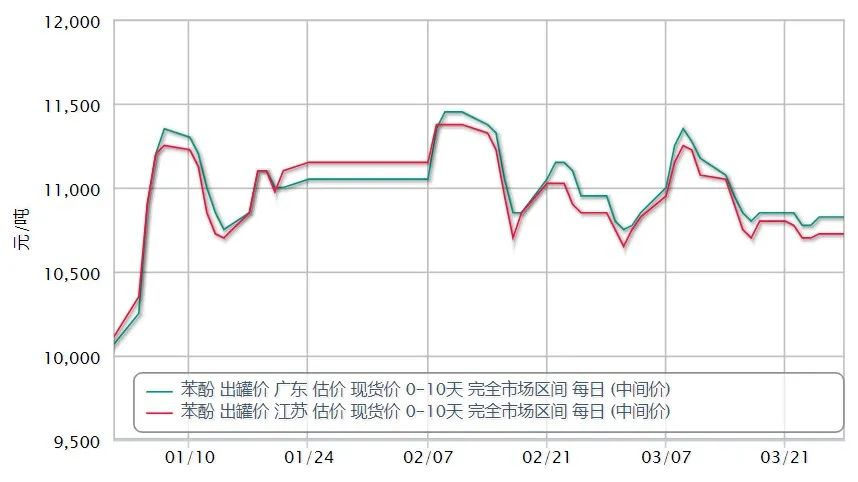

In March, the domestic phenol market first rose and then fell as a whole downward trend. 1 March domestic phenol market average offer 10812 yuan / ton, March 30 daily offer 10657 yuan / ton, down 1.43% during the month, 10 domestic phenol market offer 11175 yuan / ton, an amplitude of 4.65%. By the end of the month, the market in East China was quoted at around RMB10,650/mt, South China was quoted at RMB10,750/mt, and North China and surrounding areas in Shandong were quoted at RMB10,550-10,650/mt.

In the first half of the month, the escalation of the conflict between Russia and Ukraine to the support of soaring crude oil prices, pulling the raw material side of pure benzene, styrene and other foreign markets rose sharply, and at this time propylene rose significantly, the good increase in the center of gravity climbed higher, the phenol market upward. Subsequently, Lihua Yi and Zhejiang Petrochemical downstream bisphenol A supporting device parking, despite a slight negative but in the case of supply pressure is not much upward trend continued.

No. 10 crude oil plunge, while the domestic epidemic spread in many parts of the country, resulting in more local transportation disruptions, some downstream due to the finished product shipments are blocked, and therefore reduce the unit start-up load, thereby reducing the demand for raw phenol. Holders of shipments are blocked, the offer has loosened, the domestic pure benzene market also showed a decline in the trend, the phenol market lack of support, in response to the decline.

From March 28, the city of Shanghai is divided into areas to carry out closure control management. High bridge petrochemicals, Sinopec Mitsui and Shanghai Cesar Chemical phenol ketone plant are located in Jinshan Chemical Industry Park, due to the restrictions of the closure control management, delivery is blocked, resulting in the reduction of the spot circulation of phenol in East China.

Meanwhile, the downstream bisphenol A market as a whole downward-oriented, bisphenol A market in early March continued to fall, mainly supply and demand side are not favorable, the upstream raw materials continue to fall, while the downstream demand is difficult to talk downturn, the market once fell to 15,300 yuan / ton. But near the end of the month by the downstream PC side of the centralized replenishment demand favorable, the market rebounded, up quickly and up in 1000-1300 yuan / ton, up significantly, as of 30 domestic market mainstream quotes to 16400-16500 yuan / ton.

Throughout the second half of the epidemic caused by logistics problems more and more serious, the region's poor flow of supplies, and dual raw materials have also entered the downside channel, holding merchants under constant concessions, the market accelerated downward, the market center of gravity seriously setback. In the second half of the year, petrochemical manufacturers under pressure to focus on reducing guidance prices, but the market weakness is difficult to contain the trend, the field transactions are cold.

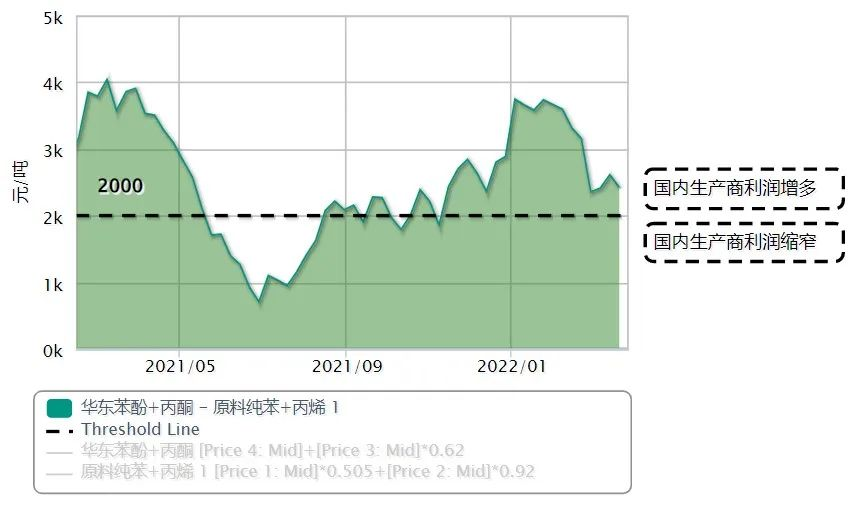

Recent high prices of crude oil, pure benzene and propylene and other upstream raw materials, domestic phenol and ketone device profitability has also shrunk significantly. Taking into account the impact of the epidemic on the market, the focus of attention will remain on the supply and demand side of the phenol market.

Supply-side concerns about the stable operation of the second phase of the phenol ketone plant in Zhejiang Petrochemical; Lihua Yiweiyuan two sets of bisphenol A plant after the resumption of normal production after parking maintenance, phenol commodity volume may be reduced; and the subsequent impact of the epidemic in Shanghai on the production of three sets of local phenol ketone plant.

Demand-side concern about the two sets of new bisphenol A device production, Cangzhou Dahua 200,000 tons / year and Hainan Huasheng 240,000 tons / year originally planned to be put into operation in April, but due to the recent spread of the epidemic, some market participants are also concerned about the commissioning time or the existence of delayed expectations.

In April, we should continue to pay attention to the logistics and transportation situation caused by the epidemic, especially in the northern region, the logistics is blocked, and the pressure on the stockholders to ship is greater, the downstream terminal enterprises at this stage just need to follow up mainly, the replenishment intention is not large. On the other hand, the recent cost side is affected by the fluctuation of crude oil. It is expected that the supply-demand balance in April will not change much, and the domestic phenol market is expected to operate in a range of fluctuations.

Jincheng Petrochemical's 300000 ton polypropylene plant successfully trial production, 2024 polypropylene market analysis

The ABS market remains sluggish, what is the future direction?

Market differentiation of bisphenol A intensifies: prices rise in East China, while prices generally decline in other regions

The production method and process flow of silicone acrylic lotion, and what are the common raw materials